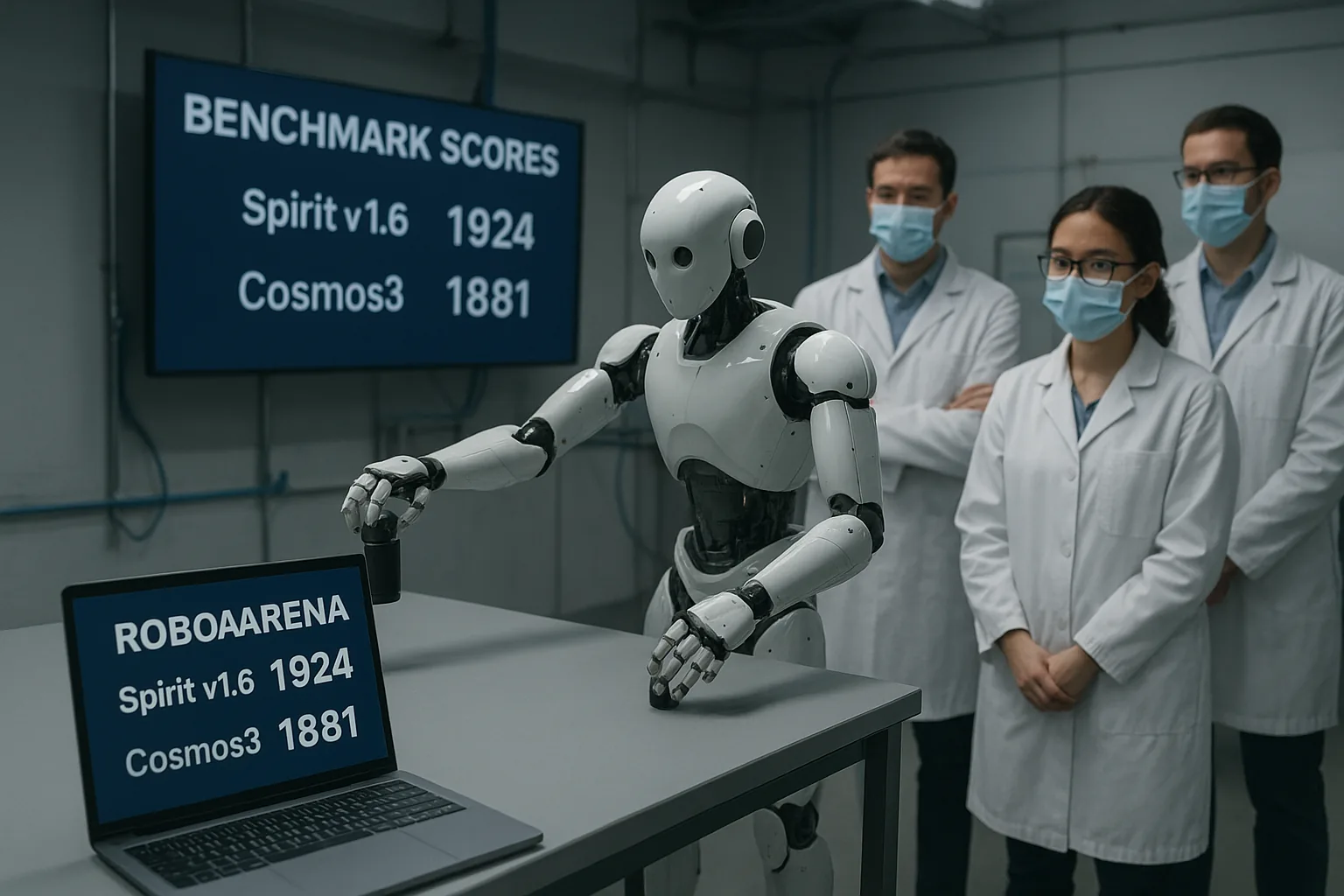

Two days after Nvidia put Cosmos 3 on stage, engineers in Hangzhou were not staging a demo — they were watching numbers change on a benchmark scoreboard. Spirit AI said Spirit v1.6 scored 1,924 on RoboArena, nudging past Nvidia's Cosmos3‑Nano‑Policy at 1,881. The win is the sort of concrete detail that punctures slide-deck narratives: it happened in public, it was measured on a benchmark co‑developed with leading labs, and Spirit announced a 1.5 billion yuan funding round the same week. That combination of performance and capital has sent a single, blunt message into the wider us-china tech war: china’s lead in embodied AI is less mystical and more material than many in the West assumed.

us-china tech war: china's robotics win is about data, not just GPUs

Spirit's scoreboard victory answers a headline question — how did China beat Nvidia in this contest? — with an operational, not mystical, explanation. Spirit did not outspend Nvidia on supercomputers; it produced a policy model that performs better in RoboArena's randomized, anti‑overfitting tests. The key ingredient is access to varied, large-scale robotics data and fast iteration loops: companies in China are collecting manipulation logs, multi‑camera footage and robot trials at industrial scale and feeding them back into foundation models. Where Nvidia and other Western groups rely on expensive GPU cycles and simulation fidelity, Chinese teams are exploiting real‑world scale and lower unit costs to close the performance gap.

This matters for robotics developers. Winning RoboArena doesn't instantly create a perfect humanoid; it lowers the engineering burden of transferring simulated behaviours into messy reality. For a developer choosing between licensing a foreign policy stack, building in‑house, or using a local provider, Spirit's result rewrites the calculus: models that have seen hundreds of thousands of real interactions will adapt with less fine‑tuning, require fewer ultra‑expensive simulation cycles, and shave months off deployment timelines.

us-china tech war: china's industrial playbook — funding, factories and regulation

There is a clear industrial playbook behind Spirit's score. The company announced a blockbuster financing round — 1.5 billion yuan this week — part of a broader sprint of capital into physical AI. Investors and local governments are pumping money into start‑ups that can demonstrate embodied capabilities, and municipal incentives are pairing cheap hardware, factory floors, and testbeds with software teams. That's the kind of vertically integrated environment the EU and the US have struggled to replicate at scale.

Regulation plays its part. China’s central and local authorities have been pragmatic about rules for piloting drones, robotaxis and other low‑altitude or urban systems. Where US litigation and fragmented state rules have slowed real‑world robot rollouts, Chinese regulators have often prioritised rapid pilots with clear operational boundaries. That reduces the time between benchmark success and a paying customer — an economic advantage that feeds back into more data, more edge cases, and thus stronger models.

From a European perspective, this creates pressure. The Chips Act and recent EU funding programmes aim to shore up semiconductor and AI supply chains, but Spirit's win shows the gap isn't just about fabs. It's a system problem: capital flows, permissive testbeds, and industrial ecosystems all matter. Europe has engineering depth; what it lacks is the single administrative mind that coordinates incentives at city and region scale — and it certainly hasn't chosen which government will underwrite the risk.

Benchmark mechanics: why RoboArena matters to engineers and policymakers

But benchmarks are also partial. A RoboArena victory signals readiness for a class of generalist tasks — manipulation, navigation, tool use — but it does not replace months of integration work on hardware, safety validation, and regulatory sign‑off. Nvidia remains dominant in many parts of the stack: chip design, data‑centre GPUs, and simulation tooling. Spirit’s win is therefore more an inflection point than a knockout.

Policymakers should notice two things: first, the bottleneck for embodied AI is increasingly data and integration capacity; second, export controls on GPUs, while bluntly effective in one domain, do not prevent performance gains achieved through different levers. That has consequences for how Western governments design industrial policy: withholding hardware can slow some actors, but it can also push rivals to innovate around constraints.

How Chinese accelerators compare to Nvidia GPUs — and why it matters for developers

The PAA question about how Chinese AI accelerators compare to Nvidia GPUs is practical and urgent. High‑end Nvidia chips remain the gold standard for raw floating‑point throughput, memory bandwidth and the software ecosystem around CUDA. Chinese accelerators — Huawei’s Ascend series, Baidu's M‑class chips and others — are catching up in sustained throughput and are often cheaper to operate inside domestic cloud stacks. They typically lag in absolute peak performance and in the maturity of developer tools, but they compensate with better local integration, regulatory clarity, and cost per training hour.

For robotics developers, the implication is straightforward: if your product needs the last 10–20% of performance for huge multi‑month model training runs, Nvidia remains the fastest path. If your priority is frequent retraining on streaming real‑world data, lower cloud costs and easier deployment inside China, local accelerators are increasingly competitive. Spirit’s result shows that clever model design and abundant task data can offset a raw‑compute deficit — a reminder that chips are necessary but not sufficient.

What this win means for the US-China tech war: tactical shifts, not instant dominance

Spirit's top ranking will be framed in many quarters as a geopolitical milestone, but the right read is more nuanced. The US still holds material advantages in advanced chip design, developer ecosystems, and leading LLM research. China holds advantages in manufacturing scale, field data collection and a single‑minded industrial policy that aligns capital, testbeds and regulators. That division — "brains" versus "bodies" in one popular shorthand — is blurring as both sides cross‑pollinate tactics.

For robotics firms worldwide, the new reality will be hybrid: adopt Western toolchains where their software and chips accelerate research, and tap Chinese models and datasets where deployments require rapid, cost‑effective scaling. For policymakers, the lesson is that export controls and sanctions are one tool among many; long‑term advantage will depend on funding, standards, and who wins the messy business of getting robots to work in the world.

Sources

- RoboArena benchmark (Nvidia, Stanford University, University of California, Berkeley)

- Spirit AI (company announcements and financing round)

- Nvidia (Cosmos 3 and related research)

- Manifold AI (WorldScape benchmark results)

- TSMC and ASML (semiconductor supply‑chain context)

- Baidu, Huawei (Chinese AI chips and industrial policy)

Comments

No comments yet. Be the first!